For many South Africans planning to relocate abroad, structuring finances ahead of departure is a critical step. But what may seem like a simple transfer of assets between spouses could now place you firmly on the radar of the South African Revenue Service (SARS).

Recent developments signal a clear shift in how donations tax in South Africa is being enforced, particularly where inter-spousal transfers coincide with plans to cease South African tax residency. If you are considering asset transfers before emigrating, it is important to understand why SARS is paying closer attention.

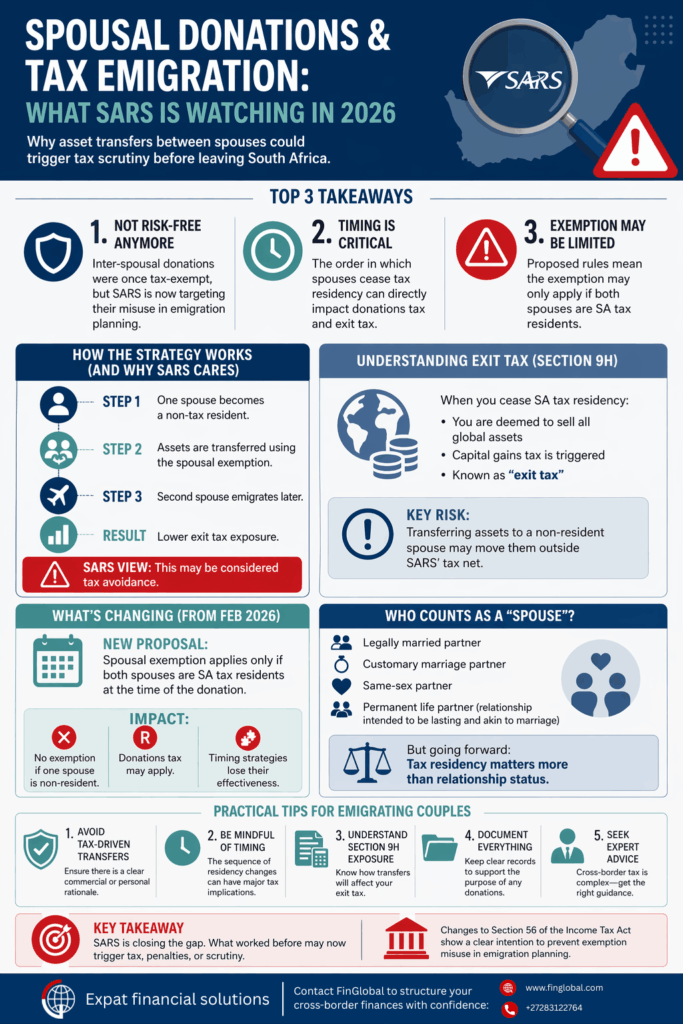

Top 3 takeaways for South Africans planning to emigrate

- Inter-spousal donations are no longer risk-free. While donations between spouses in South Africa have traditionally been exempt under section 56 of the Income Tax Act, SARS is now targeting structures that use these transfers to reduce tax before emigration. What was once standard practice may now trigger scrutiny.

- Timing your tax residency matters more than ever. The order in which each spouse ceases tax residency in South Africa can change the tax outcome. For example, if one spouse becomes a non-tax resident first and assets are then transferred between you, it could affect both the donations tax and the exit tax under section 9H of the Income Tax Act. When timing and inter-spousal transfers are used together, it may trigger unexpected tax costs or SARS scrutiny.

- New rules may limit the spouse exemption. Proposed changes to the South Africa donations tax exemption between spouses mean the exemption may only apply if both spouses are South African tax residents. If one spouse is already a non-tax resident, the donations tax could apply between spouses.

Read more: Tax planning secrets you must know before leaving South Africa.

The role of donations tax in South Africa

Under the South African Income Tax Act, donations tax applies when a person disposes of assets for no consideration or for less than market value. This includes cash, property, shares, and other financial assets.

There are, however, key exemptions. One of the most widely used is found in Section 56 of the Income Tax Act, which allows for donations between spouses without triggering donations tax. This has historically made inter-spousal transfers an attractive and legitimate financial planning tool.

In addition, individuals benefit from an income tax donation exemption, which has recently increased to R150 000 per year from March 2026. This general donation tax exemption provides some flexibility for smaller transfers.

Why SARS is tightening the rules on inter-spousal donations

The issue arises when these exemptions are used as part of broader tax planning strategies linked to emigration.

According to the 2026 Budget Review, SARS has identified cases where individuals deliberately stagger their tax evasion. In these scenarios, one spouse becomes a non-tax resident of South Africa first, and the other follows later.

During this window, assets are transferred to the already non-resident spouse using the inter-spousal tax exemption provisions. Because the donation is between spouses, it qualifies for exemption under section 56 of the Income Tax Act.

The second step is where it becomes more complex. When the remaining spouse eventually proceeds with ceasing their South African tax residency, the exit tax under section 9H of the Income Tax Act may be significantly reduced because fewer assets remain in their name.

According to SARS, this amounts to tax avoidance in South Africa.

Understanding the exit tax connection

When you cease tax residency in South Africa, you are deemed to dispose of your worldwide assets at market value. This triggers capital gains tax, commonly referred to as the exit tax, under section 9H.

Normally, donations between spouses are tax-neutral due to rollover relief. This means the receiving spouse inherits the base cost of the asset, and tax is deferred until a future disposal.

However, when assets are transferred to a spouse who is already a non-tax resident of South Africa, those assets may effectively fall outside the SARS tax net. This undermines the intent of the system, which is to ensure tax is eventually collected.

This is precisely the gap SARS is now looking to close.

Read more: Understanding South Africa’s exit tax – a guide for expats.

Proposed changes to section 56 of the Income Tax Act

To address this, the government has proposed an amendment to section 56 of the Income Tax Act.

From 25 February 2026, the donations tax exemption between spouses or life partners will only apply if both spouses are South African tax residents at the time of the donation.

This means:

- The donations tax exemption will no longer apply where one spouse is already a non-resident

- Donations tax between spouses could become payable in these cases

- Timing strategies involving staggered residency may lose their effectiveness

This change directly targets the misuse of inter-spousal transfers in emigration planning.

Who or what counts as a “spouse”?

It is also important to understand the definition of spouse in South African law. For tax purposes, a spouse includes:

- A legally married partner

- A partner in a customary marriage

- A partner in a same-sex union

- A partner in a permanent life partnership, where the relationship is intended to be lasting and akin to marriage

This broad definition means that the South African donations tax exemption between spouses applies to a wide range of relationships. However, under the proposed changes, tax residency status will become the determining factor — not just the relationship itself.

Is this a widespread issue?

Interestingly, SARS has indicated that this practice is not widespread. It has mainly been observed among high-net-worth individuals engaging in sophisticated tax structuring.

However, the fact that it has been singled out in policy discussions shows that SARS considers it significant enough to act on. Even if you are not intentionally engaging in aggressive tax planning, poorly timed or undocumented asset transfers could raise questions.

Practical guidance for emigrating couples

If you are planning to cease tax residency in South Africa, careful planning is essential. Here are some key considerations:

- Avoid making purely tax-driven transfers. Asset transfers that lack a clear commercial or personal rationale may be viewed as tax avoidance.

- Be mindful of timing. The sequence in which spouses change their tax resident status can have significant tax implications.

- Understand section 9H exposure. Before transferring assets, consider how this will affect your exit tax under section 9H of the Income Tax Act.

- Document everything. Clear documentation supporting the purpose of any donations between spouses in South Africa can help demonstrate legitimacy.

- Seek professional advice. Cross-border tax planning is complex, particularly when dealing with donation tax in South Africa and tax emigration. Expert assistance can help you avoid stress by ensuring tax compliance.

FinGlobal: cross-border tax specialists for South Africans

FinGlobal: cross-border tax specialists for South Africans

The rules around donations tax in South Africa are tightening, and what was once a straightforward financial strategy between spouses is now firmly on SARS’ radar. Changes to section 56 of the Income Tax Act highlight a clear intention to prevent exemption misuse, particularly where ceasing South African tax residency is involved.

For future expats, this means one thing: careful planning is critical. The interaction between inter-spousal transfers, donations tax, and exit tax under section 9H of the Income Tax Act is complex, and getting it wrong can be costly.

FinGlobal specialises in helping South Africans structure their affairs correctly — from tax emigration, retirement annuity withdrawal, and SARS tax clearance to seamless foreign exchange — so you can move abroad with certainty and peace of mind.

Don’t take chances — contact FinGlobal today to ensure your tax emigration and cross-border finances are structured correctly from the start.