Many South Africans working abroad assume that earning an income overseas automatically means they no longer have to pay tax in South Africa. Unfortunately, that’s not always true.

Whether you work on a cruise ship, as yacht crew, on offshore oil rigs, or as part of an international shipping operation, the South African Revenue Service (SARS) may still expect you to declare your foreign earnings and, in some cases, pay tax on them too. This often surprises South Africans employed under international crew visas or paid into offshore bank accounts.

However, where you are paid or which currency you earn in does not determine your tax obligations. What matters is your tax residency status, whether you qualify for a specific exemption, and how South Africa’s tax laws and treaties apply to your situation.

Three key things South Africans working offshore need to know about seafarers’ tax

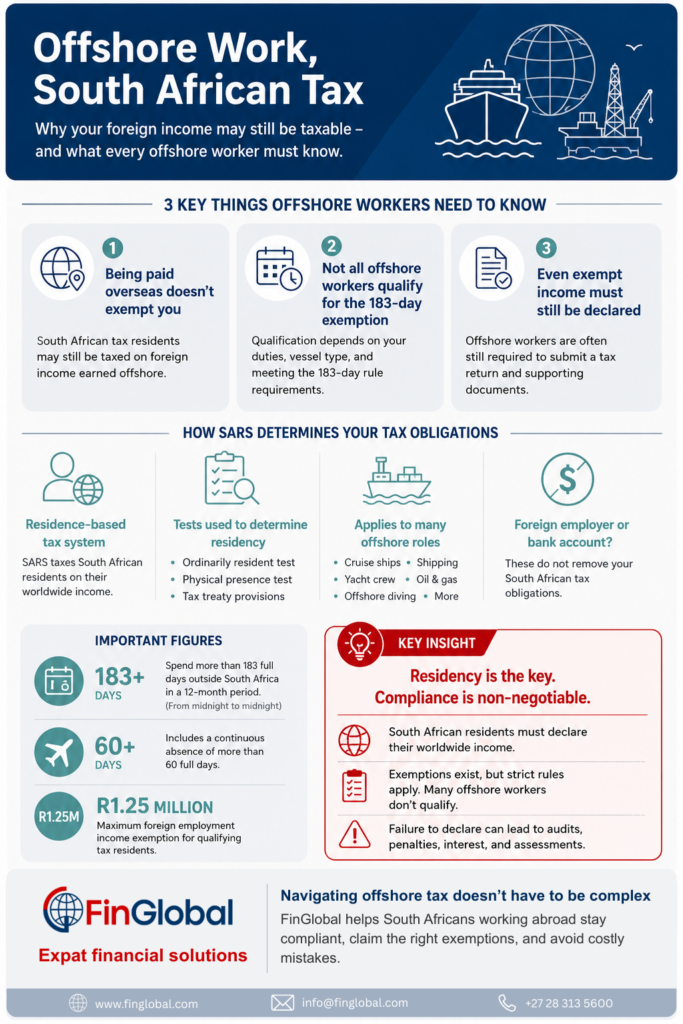

- Being paid overseas does not automatically exempt you from SARS. South African tax residents may still be taxed on foreign income earned offshore.

- Not all offshore workers qualify for the 183-day tax exemption in South Africa. Qualification depends on your duties, vessel type, and meeting the 183-day rule requirements.

- Even exempt foreign income must still be declared to SARS. Offshore workers are often still required to submit a tax return and supporting documents.

Why SARS may still tax South Africans working abroad

South Africa uses a residence-based tax system. This means South African tax residents are generally taxed on their worldwide income, regardless of where they earn it.

Under the Income Tax Act of South Africa, SARS first determines whether you remain a South African tax resident. This is assessed using:

- The ordinarily resident test

- The physical presence test

- Applicable tax treaty provisions

If you are still considered a South African tax resident, SARS may tax your foreign earnings unless you qualify for a specific exemption. This catches many offshore workers off guard, especially those working in:

- Cruise ship operations

- Commercial shipping

- Yacht crew employment

- Offshore diving

- Oil and gas support services

Many workers incorrectly assume that having a foreign employer or offshore bank account removes their South African tax obligations. In reality, SARS focuses on tax residency and the nature of your work.

Understanding the seafarer tax exemption

The seafarers tax exemption South Africa is one of the most misunderstood areas of offshore taxation. The exemption falls under section 10(1)(o)(i) of the Income Tax Act and may allow qualifying South African seafarers to receive a full tax exemption on foreign employment income.

To qualify for the seafarer tax exemption, several conditions usually apply:

- You must be employed onboard a qualifying vessel

- The vessel must operate in international transport

- Your duties must be performed “on board for the passage” of the vessel

- You must spend more than 183 full days outside South Africa

This is why understanding SARS section 10(1)(o)(i) is so important for offshore workers.

Read more: Seafarers tax relief in South Africa: avoiding common offshore compliance mistakes.

Why many yacht crew and offshore workers do not qualify

A major issue is that many offshore workers do not satisfy the “passage duties” requirement. For example, yacht crew, divers, riggers, and certain support contractors often perform duties that SARS may not consider directly related to the passage of the vessel itself.

As a result, they may fail to qualify for the full seafarers exemption even if they spend most of the year outside South Africa. This is particularly common in the superyacht industry, where workers may spend long periods docked in marinas rather than actively engaged in international transport.

Read more: Sail away – the yachtie’s guide to South African seafarers tax.

How the foreign employment income exemption works

For offshore employees who do not qualify for the seafarers tax exemption South Africa, the foreign employment income exemption may still offer partial relief.

This exemption allows qualifying South African tax residents to exempt up to R1.25 million of foreign employment income from South African tax.

To qualify, you must meet both:

- The 183 day rule

- The continuous 60-day absence requirement

Under the 183 day rule in South Africa, you must spend more than 183 full days outside South Africa during a 12-month period, including a continuous absence of more than 60 full days. Importantly, only full days spent outside South Africa count. SARS calculates this from midnight to midnight. Leaving South Africa even one day too late can result in falling short of the required number of qualifying days and losing access to the exemption entirely.

Read more: 183 days, 60 days, and endless confusion: your simple guide to SARS’ time rules.

Why tax treaties matter

A South Africa tax treaty can also affect where offshore workers pay tax. For example, if you work onboard a ship operated by a UK-based company, the South Africa-UK tax treaty may assign taxing rights differently depending on:

- Where the employer is resident

- The type of vessel

- The nature of the employment

- Whether the ship operates in international traffic

In some cases, tax may become payable overseas first, while South Africa may provide a foreign tax credit. This is why offshore workers should never assume that foreign payroll deductions automatically satisfy their South African obligations.

Read more: How South African expats can safeguard their foreign employment income abroad.

Contractors face additional tax complexity

Independent contractors working offshore often face additional complications. Unlike employees, contractors do not qualify for the seafarer tax deduction or foreign employment income exemption at all.

Instead, they may need to assess source-based taxation, foreign tax exposure, treaty relief options and exchange control implications. This makes professional tax guidance particularly important for consultants and freelancers operating internationally.

Read more: What is the SARS foreign income exemption, and can you use it?

You may still need to submit a tax return

One of the biggest misunderstandings around seafarers income tax is the belief that exempt income does not need to be declared. In reality, offshore workers still need to ensure that they:

- Register as taxpayers

- Declare foreign income

- Submit annual returns

- Claim exemptions correctly

- Apply for foreign tax credits where applicable

Failure to declare foreign income properly can trigger:

- SARS audits

- Administrative penalties

- Estimated assessments

- Interest charges

Good record keeping is essential. SARS may request travel records, contracts, passport stamps, payroll records, and vessel details to verify exemption claims.

FinGlobal: cross-border tax specialists for South Africans

FinGlobal: cross-border tax specialists for South Africans

Unsure how your offshore income affects your South African tax obligations? FinGlobal helps South Africans working abroad manage complex cross-border tax matters with confidence. Whether you need assistance with South African tax residency, offshore income exemptions, SARS compliance, foreign tax credits, or tax emigration, our experienced team can help you stay compliant while avoiding costly mistakes.

Speak to us today for a free consultation or leave your details below and we’ll contact you to discuss the right solution for your situation.